A. The Resource Boom and the Green Agenda

The world is witnessing an unprecedented surge in demand for resources—oil, gas, uranium, base metals, and even so-called “renewables”—to power the relentless march of digitization, artificial intelligence (AI), data centers, and robotics. This technological revolution, often championed by progressive elites, is exposing the glaring hypocrisy of green advocates who push for a “clean” future while ignoring the “inconvenient truth” that their vision requires a mining and energy revolution rooted in the very fossil fuels and commodities they like to demonize.

The rise of AI and robotics is transforming industries, from manufacturing to healthcare. Data centers, the backbone of this digital age, are being built at a record pace in order to process the vast computational needs of AI models like those powering ChatGPT or autonomous systems. These facilities consume electricity—often terawatts annually—relying heavily on oil, gas, and coal to keep the lights on. In 2024, global data center energy consumption was estimated at 460 TWh, projected to double by 2030. Meanwhile, electric vehicles (EVs), robotics, and smart grids demand batteries and infrastructure loaded with copper, lithium, cobalt, and rare earths. Even Uranium, is seeing a renaissance as nuclear power gains traction to meet baseload energy demands. Our so-called green utopia it actually turning out to be a resource-hungry steamroller.

The irony is thick. Green advocates, from Leonardo DiCaprio to Greta Thunberg, lecture the world on climate change while drinking soymilk lattes from Starbucks powered by fossil fuels and coal powered power plants and tweeting from smartphones built on the backs of child labour working in strip-mining cobalt and lithium mines. Their push for renewables, including solar panels, wind turbines, and EV batteries requires an explosion in mining over the next two decades. A single wind turbine needs tons of steel, copper, and rare earths, often sourced from environmentally destructive operations in places like China or Congo. EVs require three times the copper of gas-powered cars, and lithium demand is projected to surge 40% by 2030. Yet, these same advocates vilify miners, oil drillers, and pipeline workers as planet-killers, while conveniently ignoring the strip-mined damage that is fueling their net zero 2050 fantasies. A single ChatGPT query consumes approximately 2.9 watt-hours of electricity, nearly 10 times the 0.3 watt-hours required for a Google search. With over 400 million active ChatGPT users weekly, this scales to a massive energy footprint.

This hypocrisy exposes a deeper truth: the green agenda is a smokescreen. The left’s obsession with renewables has very little to do with saving the planet and more to do with top-down control over the lives of people. Oil and gas, the lifeblood of our economy, employs millions (directly and indirectly) and keeps our energy costs low, a key component to maintaining our competitiveness as a country. Yet the Trudeau (Carney) administration choked pipelines while green proponents cheered. Bill C-69 which passed in 2018 has chased billions of investments out of Canada by creating an overly complex, uncertain, and lengthy regulatory process that prioritizes to the extreme environmental and social considerations over economic development and growth. Opposition parties in Canada point to a $500 billion net outflow of investment capital from Canada to the US since 2015 as evidence of the economic carnage caused by policies like Bill C-69 and other government overreach.

Meanwhile, their AI-driven tech utopia demands more fossil fuels, base metals and rare earths than ever. The International Energy Agency warns that achieving net-zero by 2050 requires a sixfold increase in critical mineral production—hardly the eco-paradise they peddle.

We see through this charade. We champion energy independence, not reliance on Chinese-controlled rare earths or unstable foreign regimes. Domestic oil, gas, and uranium can power our tech revolution while keeping jobs in North America and especially in Canada. Mining, too, can be done responsibly within our own country, not outsourced to communist polluters abroad. Green advocates can’t have it both ways—pushing AI and EVs while demonizing the resources that make them possible. It’s time to embrace our energy might, unleash our miners, and build a future that’s strong, not woke.

Canada with its vast natural resources should be one of the world’s wealthiest nations. Our abundant reserves of oil, natural gas, and minerals like gold, nickel, and uranium should be fueling a vigorous export economy that goes well beyond the US. Canada’s extensive forests along with our fertile lands should be supporting a massive timber and agricultural goods export boom to global markets. Canada’s freshwater resources and hydroelectric potential provide renewable energy at some of the lowest costs anywhere in the world, while reducing our reliance on costly imports.

What Canada needs is leadership. Leadership and wisdom are crucial for a nation’s prosperity, “without vision, the people perish” (Proverbs 29:18). Wise leaders are those who are guided by the fear of the Lord and pursue justice and impartiality. As Solomon reminds his readers, “the fear of the Lord is the beginning of wisdom” (Proverbs 9:10). Without principled leadership, societies crumble, “when the righteous increase, the people rejoice, but when the wicked rule, the people groan.” (Proverbs 29:2). Godly leadership fosters peace and progress because it aligns decisions with moral truth. The groaning in Canada today is because we have wicked men and women ruling over us.

B. North American Equity Market Statistics

Canadian Equities

In Q2 of 2025, the Canadian equity market, as measured by the S&P/TSX Total Return Index, rose 7.78%. Over the past year, the index gained 22.77%, including dividends. Our portfolio of Canadian companies, net of fees, increased 12.01% during the quarter and 32.7% over the past 12 months, outperforming the index by approximately 10%. Over the past five and ten years, our Canadian holdings achieved annualized returns of 9.5% and 10.7%, respectively. Compared to the S&P/TSX, we underperformed by 2.1% annually over five years but outperformed by 4.4% annually over ten years.

Our significant allocation to precious metals royalty companies was the primary driver of our outperformance. We remain confident in our core holdings and their strong long-term fundamentals. Our direct exposure to tariffs and trade tensions is minimal. Amid heightened tariff concerns, we are focused on protecting capital and seizing opportunities. As we enter Q3, stock markets are at all-time highs and may be susceptible to a correction.

In terms of the S&P/TSX index, all eleven sub-sectors generated positive returns during the Q2. The returns of the sub-sectors from highest to lowest are: Information Technology (+14.2%), Consumer Discretionary (+13.4%), Financials (11.1%), Industrials (+7.8%), Materials (+7.7%), Consumer Staples (+4.3%), Real Estate (+3.9%), Utilities (+3.7%), Health Care (+2.4%), Communication Services (+1.0%) and Energy (+0.1%).

US Equities

In Q2 2025, our portfolio of U.S. and global companies, net of expenses, grew by 3.31% in Canadian dollars and 9.04% in U.S. dollars. Over the past 5 and 10 years, our portfolio achieved annualized returns of 9.0% and 12.7%, respectively. The companies we own offer strong fundamentals, above- average growth, and reasonable valuations. Over the past 5 years, our performance trailed the S&P 500 by 7.5%, and over 10 years, we underperformed it by 0.9%. However, we outperformed the Dow Jones Industrial Average (DJIA) by an annualized 3.1% and the Russell 2000, a small-cap index, by 7.0% over the same 10-year period.

Recent U.S. market returns have been driven by a small group of highly valued companies, fueled by enthusiasm for digitization and artificial intelligence (AI). While these trends are transformative, we remain disciplined, avoiding overvalued securities and speculative investments to deliver consistent, long-term returns for our investors. Given the scale of the U.S. market, most new holdings added to our portfolios in the past 2–3 years have been U.S.-domiciled global businesses. We typically adjust our portfolio by adding or removing 2–3 companies annually. In Q1 2025, we added Kelly Partners Group Holdings, which was discussed in our Q1 2025 newsletter.

Market Statistics

Pertinent market action during the Q2 of 2025 and during the last 12 months is captured in the following table.

| June 30, 2024 | Mar. 31, 2025 | June 30, 2025 | 3 Month Return | 1 Year Return | |

| CAD/USD | $0.7307 | $0.6951 | $0.7349 | +5.72% | +0.57% |

| Oil WTI (US $) | $81.52 | $71.37 | $65.11 | -8.77% | -20.13% |

| Gold (US $) | $2,323.39 | $3,123.96 | $3,303.14 | +5.73% | +42.17% |

| Silver (US $) | $29.10 | $34.06 | $36.11 | +6.02% | +24.09% |

| S&P/TSX | 21,893 | 24,917 | 26,857 | +7.78% | +22.67% |

| S&P 500 | 5,460 | 5,612 | 6,205 | +10.57% | +13.64% |

| Cdn 10 yr. | 3.50% | 2.97% | 3.31% | +34 bps | -19 bps |

| US 10 yr. | 4.38% | 4.21% | 4.23% | +2 bps | -15 bps |

During the Q2 of 2025, the Canadian dollar (CAD) appreciated by 5.72% against the U.S. dollar (USD) and gained 0.57% over the past twelve months, recovering from a recent low of 67–68 cents USD in February 2025. Political uncertainty, including the 2024 resignation of Finance Minister Chrystia Freeland, and concerns over potential U.S. tariffs under President-elect Donald Trump, combined with economic challenges, have pressured the CAD. Historically, when the CAD falls below 70 cents USD, it often rebounds, provided Canada’s economic and political conditions stabilize. The CAD has traded below 70 cents USD several times over the past 50 years, driven by economic, political, and commodity price volatility:

- 1974–1982: High inflation, rising interest rates, and political uncertainty, particularly after the 1976 election of René Lévesque in Quebec, led to a CAD low of 69.13 cents USD in November 1976

- 1986: The CAD briefly dipped below 70 cents USD due to global economic conditions and low commodity prices.

- 1998–2002: Weak commodity prices, especially oil, a strong U.S. economy and a mismanaged federal government debt crisis pushed the CAD to a low of 61.79 cents USD in January 2002.

- 2016: A sharp decline in oil prices drove the CAD to 68.68 cents USD on January 19, 2016.

- 2020: The CAD fell below 70 cents USD in March 2020 amid economic uncertainty from the COVID-19 pandemic.

- 2024–2025: Political instability and U.S. tariff threats led to the CAD dropping below 70 cents USD on December 17, 2024, reaching 67–68 cents USD in February 2025.

Canada’s economy is facing challenges, prompting the Bank of Canada to cut interest rates more aggressively than the U.S. Federal Reserve, with the current rates at 2.75% and 4.25%, respectively, resulting in a 1.5% gap. This has further weakened the Canadian dollar against the USD. Due to ongoing unfavorable economic and social policies from Ottawa, we remain cautious about Canada’s outlook and are diversifying your investments into global businesses to mitigate CAD risk.

In Q2 of 2025, gold rose 5.73%, reaching $3,303 per ounce, with a 42.17% gain over the past year. Silver increased 6.02% in the quarter and 24.1% annually. We are optimistic about the long-term potential of precious metals and continue to finetune our positions in this sector. While prices may stabilize in the near term, many precious metals mining and royalty companies are attractively valued. These businesses are well-positioned to benefit from global instability, tariff changes, government over-spending, and rising precious metals prices. Year-to-date, the stock performance of our key holdings includes Franco-Nevada (+40.4%), Gold Royalty (+90.1%), Osisko Royalties (+43.8%), Royal Gold (+36.4%), Sandstorm Gold (+72.6%), Wheaton Precious Metals (+61.0%), and Agnico Eagle Mines (+53.5%).

Few realize that gold has outperformed the S&P 500 total return index over the past 25 years. From January 1, 2000, to June 30, 2025, gold’s price rose from $290 to $3,303, yielding a compound annual growth rate of 10.33%. In contrast, the S&P 500, with reinvested dividends, achieved a 7.14% annual growth rate. This comparison highlights the impact of excessive financialization, money printing, massive debt, and low interest rates. These policies have all failed to create broad, sustainable wealth. Gold, undeterred by these policies, has proven a reliable store of value. John Maynard Keynes called the gold standard a “barbarous relic,” but his blind trust in state-controlled fiat currency, shared by many economists, eventually leads to currency devaluation because of government corruption. Because we have no confidence in any government nor in any of the Western central banks, we continue to invest in precious metals, either directly or through royalty and mining companies.

In the Q2 of 2025, oil prices fell 8.77%, with a year-over-year decline of 20.13%. Concerns about tariffs and slower economic growth have pressured oil prices, which are seeking a bottom. Following Donald Trump’s election, we expect increased U.S. oil and gas exploration, development, and production, likely capping prices in the coming years. Consequently, our direct exposure to the oil and gas sector remains minimal, with investments comprising less than 1% of total assets.

During the same period, interest rates rose slightly amid inflation concerns and a resilient U.S. economy. The 10-year Canadian bond yield increased by 34 basis points, while the U.S. 10-year Treasury yield rose by 2 basis points. Year-over-year, yields have declined by 19 basis points for Canadian bonds and 15 basis points for U.S. bonds. We continue to invest in 1–3-year bonds, balancing attractive interest rate returns with low price volatility.

C. ROCKLINC Investment Update

Private Client Assets – Separately Managed Accounts

Our ROCKLINC separately managed accounts delivered a 2.64% return in Q2 and a 15.03% return over the past year (ending June 30, 2025). More significantly, our average annual compound returns over the past 3, 5, and 10 years were approximately 9.4%, 6.6%, and 8.2%, respectively. These returns are net of fees and reflect an asset allocation of approximately 68% in equities, with the balance in short term deposit accounts and short-term bonds. Please note that these figures represent aggregate performance across all accounts. Individual client portfolios may vary based on risk tolerance and specific asset allocations.

Our equity portfolio (comprising Canadian, U.S., and global equities) achieved an 8% return in Q2 and a 22% return over the past 12 months. Over the past 5 and 10 years, our equities have compounded at approximately 10% and 11.4% annually, respectively, aligning with major market indices. Our investment approach remains focused on the economic fundamentals of the businesses we own. We prioritize:

- Selectively adding companies identified through our research team’s analysis.

- Divesting underperforming businesses.

- Capitalizing on market volatility to increase positions at attractive prices.

In Q1 we added Kelly Partners Group to our portfolios, as noted in our previous report. No new positions were added in the Q2, but we are actively monitoring several companies for potential investment at optimal valuations.

ROCKLINC Partners Fund

Over the past four years, we have been utilizing the Partners Fund in more of the portfolios we manage. The Fund offers our clients a low cost and efficient way to purchase our top 20-25 companies in one portfolio. It is an effective way to gain access to a global diversified portfolio with modest amounts of investment capital. Our number one objective is to create a Fund comprised of excellent companies that produce strong long-term performance.

Quarterly, we provide a performance update to our clients. Performance numbers are after all fees and rates of return beyond one year are annual compound rates of return. Currently, the Fund is 15% in cash and short-term money market instruments (yielding 2.5 – 3%), 83.5% in publicly traded equities and 1.5% in two private equity investments. We expect our cash weighting to remain in the 15-20% range given market valuations. We finished the quarter with $57 million in total assets, up from $46 million at the beginning of the year and $52 million at the end of March.

During Q1, we sold two businesses—MEG Energy and Progressive Corp—and added one new business, Kelly Partners Group. In Q2 we invested in our second private company Protexxa Inc. The company was founded by CEO Claudette McGowan in 2021. It is a Canadian B2B SaaS cybersecurity company that leverages AI through its Protexxa Defender platform to identify, evaluate, and resolve cyber issues, focusing on personal cyber hygiene to mitigate business risks. Cybersecurity is a growing industry due to the increasing frequency and sophistication of cyber threats, driving demand for advanced security solutions. We will have more to say about this company in future newsletters and look forward to interviewing Protexxa’s CEO Claudette McGowan for distribution to our clients.

As new money flows into the Fund, we will add to existing positions based on the valuations of the companies in the portfolio.

After all expenses, the ROCKLINC Partners Fund has been compounding at approximately 8.3% per year since inception (September 29, 2017) and by 12.1% and 6.4% over the past three and five years.

Over the past three years, the portfolio’s Canadian equities have compounded at 12.6%, while U.S. equities have compounded at 17.5%. Since inception in September 2017, Canadian equities have returned 11.5% annually, and U.S. equities have returned 12.0%. The Canadian holdings have consistently outperformed the S&P TSX since inception. The U.S. holdings have slightly underperformed the S&P 500 but have significantly outperformed the DJIA and Russell 2000.

Our top 12 holdings represent approximately 65.5% of the total portfolio and 77% of the equity weighting in the portfolio. The top 12 holdings are Trisura Group (10.5%), Brookfield Corporation (8.5%), Markel Group (7.4%), Wheaton Precious Metals (5.5%), Amazon (5.5%), Franco-Nevada (4.9%), Kelly Partners (4.8%), Burford Capital (4.3%), Sandstorm Gold Royalties (4.0%), Cameco Corp (3.6%), API Group Corp (3.4%) and Roper Technologies (3.1%).

As at June 30, 2025

| 3 mos. | 6 mos. | 1 yr. | 3 yr. | 5 yr. | Inception* | |

| RL Partners | 8.1% | 8.9% | 18.2% | 12.1% | 6.4% | 8.3% |

ROCKLINC Kokomo Fund

In November 2022, we introduced the ROCKLINC Kokomo Fund to offer our clients a regulated investment product registered outside Canada. The fund is domiciled in the Cayman Islands, a leading British Overseas Territory and the world’s premier offshore market for investment funds, with all assets securely held in custody in Grand Cayman.

The ROCKLINC Kokomo Fund is supported by a robust team of professionals: FundBank serves as the Fund Custodian, SGGG Fund Services (Cayman) Inc. acts as the Fund Administrator, Carey Olsen provides legal counsel, and Grant Thornton (Cayman) is the Fund’s Auditor. The minimum investment is $100,000 USD, with the Net Asset Value (NAV) priced monthly, starting at $100.00 per unit. The portfolio is managed consistently with our discretionary accounts, comprising 20-25 stocks, low turnover, a competitive management fee, no performance fees, and monthly pricing and liquidity. Offering documents are available on our website or by contacting ROCKLINC directly.

We began investing in the portfolio in February 2023 and continue to gradually build our core positions. As of June 30, 2025, the Fund’s total value was approximately $7.43 million USD, with units closing at $121.78 at the end of Q2. The Fund has achieved a year-to-date return of 11.97% and an annualized return of 8.83% since inception. Consistent inflows have enabled us to increase existing positions, reduce underperforming holdings, and introduce new investments. Strong client interest continues, with new clients regularly joining the portfolio.

As of June 30, 2025, the portfolio holds 19 equity positions, accounting for approximately 85% of its total asset value. The remaining 15% is invested in a money market fund yielding about 4.5% annually. Our goal is to maintain 18–24 equity positions, with equity exposure between 85–90%, depending on buying opportunities and valuations. We are gradually increasing equity holdings while retaining cash reserves. Year-to-date we added one new position, Kelly Partners Group.

D. Company Update – Cameco Corporation (CCO)

The Emergence of a Nuclear Renaissance

Many Europeans were rudely awakened to sky-high energy bills as electricity prices reached record levels in 2022. Some countries, such as Romania, saw their electricity bill increase over 100%! The Russia-Ukraine war had left Europe scrambling to find reliable sources of base-load energy to replace the natural gas flowing from Russia. Up until this point, the European Union had been weaning itself from coal, while ramping up its renewable energy infrastructure, such as wind and solar, as part of its climate change policies. The energy crisis that ensued from the Russia-Ukraine war helped demonstrate that climate change ideology had left Europe’s energy system grossly vulnerable and ill-equipped to sustainably meet its own energy needs. The European Union was quickly confronted with the reality that it could not meet its climate change goals solely by using intermittent and weather-dependent renewable energy sources, such as solar and wind.

Similarly, California – North America’s leader in embracing climate-change policies – has faced significant challenges in its transition to renewable energy. From 2011 to 2019, electricity prices in California surged over sixfold as the state increasingly relied on renewables. For instance, prolonged droughts have impeded energy supply coming from hydropower power, while solar is not adequate to provide power during the evening time1. So how can countries transition away from using fossil fuels while simultaneously producing sufficient energy for their citizens? Turning to nuclear energy is becoming a significant part of the answer.

The nuclear power industry is undergoing a renaissance as nations increasingly embrace nuclear energy to address the climate change challenge. Nuclear power provides reliable, 24/7 baseload energy with near-zero carbon emissions, unlike weather-dependent renewable sources such as solar and wind. Many countries are extending the operational life of existing reactors and investing in new nuclear capacity. For example, Japan has restarted 14 reactors since 2015, while Italy is exploring lifting its nuclear ban. At the 2023 UN World Climate Action Summit, 31 nations across four continents, including the United States, Canada, the United Kingdom, France, the United Arab Emirates, and the Netherlands, pledged to triple global nuclear energy capacity by 2050.

The next wave of growth for nuclear energy will likely come from power-hungry data centers. According to the International Energy Agency, energy consumption from data centers is expected to account for about half of the electricity growth in the United States until 2030. In particular, energy demand from data centers that are designed for Artificial Intelligence (AI) is expected to increase 4 times by 2030. AI is increasingly becoming embedded in all forms of enterprise and consumer applications and tools, from chat bots to data analysis and internet search. Many of the leading technology and cloud computing companies have caught on to the reality that they will need an un-interrupted baseload energy to supply its data centers. Meta, which is the parent of Facebook, WhatsApp and Instagram, has signed a 20-year nuclear power purchase agreement with Constellation Energy that is expected to begin in June 20272,3. Similarly, Microsoft signed a 20-year nuclear power purchase agreement from Constellation Energy, which would involve restarting a nuclear reactor at Three Mile Island. The nuclear unit would provide 835MW of electricity, which is enough to power ~700,000 homes.4,5

Safety has been a prevailing concern of using nuclear energy. Harrowing flashbacks of major reactor accidents from Three Mile Island (USA in 1979), Chernobyl (Ukraine 1986) and Fukushima Daiichi (Japan 2011) have left a taste of public distrust in nuclear energy over the years. Following these incidents, there has been a major overhaul in nuclear regulations from advancements in safety protocols to waste management practices. For example, new nuclear facility designs have incorporated appropriate safety measures to prevent the risk of nuclear reactor cooling systems from failing. New technologies are also being developed to better handle waste. A Canadian company called Moltex is developing a fuel recycling technology that can repurpose previously used fuel for new uses6. Other technology, such as Small Modular Reactors (SMRs), are being developed to offer nuclear energy at a smaller scale with less waste than traditional nuclear reactors. An example of this is Amazon who has signed 3 new agreements with Dominion Energy to develop several SMR reactors to power its data centers7. Countries, such as France, which generates 70% of its electricity from nuclear power, has shown that it can safely use nuclear power over several decades.

Uranium – A Critical Commodity

Uranium is the primary fuel for nuclear reactors, sourced through short-term spot markets or long- term contracts. After the 2011 Fukushima Daiichi disaster, public opposition led many countries to scale back nuclear energy programs, causing a sharp decline in uranium demand and prices over the next decade. Low prices discouraged uranium miners from investing in new production, as it was economically unviable. This decade of underinvestment and reduced output has created a significant supply-demand imbalance. Current uranium production falls short of the needs of utilities to fuel their reactors, driving prices to levels that now incentivize miners to ramp up production. Additionally, utilities are increasingly wary of relying on Russian uranium supplies, further tightening the market. Developing new mines, however, is a lengthy process, often taking 10 to 15 years, which exacerbates the supply deficit. As a result, existing uranium miners are well-positioned to capitalize on these favorable market dynamics.

Cameco – A World Class Uranium Producer

Cameco is the 2nd largest uranium producer in the world with ~17% market share, preceded by Kazatomprom, which has ~20% market share. Cameco offers an attractive pure-play opportunity to invest in the high-demand for nuclear energy within the safe jurisdiction of Canada.

It has a diversified uranium business due to its vertically integrated business model. It provides fuel products and services across the nuclear fuel cycle from exploration, mining, milling, refining and conversion. Cameco has some of the world’s best grade and lowest cost mines in the world. It operates tier 1 mines that have a licensed capacity to annually produce over 30 million pounds of uranium, which can be used to power millions of homes each year. It is the world’s third largest company based on reserves with over 457 million pounds of proven and probable uranium reserves. Two of its world-class production mines are located in northern Saskatchewan. McArthur River is the world’s largest high-grade uranium mine and mill that has an expected mine life of until 2043. In 2024, Key Lake mill set a new world record for annual production. Cigar Lake is the world’s second largest high-grade uranium mine that has an expected mine life of until 2036. Both mines have uranium grades (concentration of uranium) that significantly surpass that of its competitors.

For instance, Cigar Lake has proven grades of 16.68% and McArthur River has proven grades of 6.81%, while its next largest competitor, Kazatomprom, has average grades of only 0.04% to 0.10%. This divergence in grades demonstrates the quality of Cameco’s world-class assets. To further supplement its own home-grown uranium, Cameco has partnered with Kazatomprom on a joint venture, which gives Cameco uranium production from Kazakhstan. Cameco will build long-term contracts by layering in volumes over time. Its customer contracts have a mix of base-escalated pricing and market related pricing (floor and ceilings) that enables it to benefit from increasing uranium prices, while also having downside protection when the uranium price decreases.

Cameco has a strong pipeline of long-term customer commitments which provides greater visibility and predictability of the business. For instance, Cameco has commitments to provide an average of 28 million pounds of uranium per year from 2025 to 2029, in addition to ongoing discussions with existing and prospective customers to grow its contract pipeline.

Cameco complements its nuclear value chain with its Fuel Services and Westinghouse Electric businesses. Cameco is the world’s largest commercial uranium refinery. Its commercial refinery has about 21% of the world’s uranium primary conversion capacity. The Port Hope Conversion Facility is one of only four commercial suppliers of uranium hexafluoride, which is used in uranium enrichment, in the western world.

In November 2023, Cameco entered into a strategic partnership with Brookfield Renewable Partners to acquire a 49% ownership of Westinghouse Electric. Westinghouse Electric develops nuclear reactor facilities and technology. It designs and fabricates highly engineered bespoke nuclear reactors. For instance, Westinghouse develops SMR technology that uses the same technology as its larger nuclear facilities. Complementing its nuclear asset business, Westinghouse has a nice recurring revenue business by offering aftermarket products and services, such as engineering and outage and maintenance services. This enables the company to have a predictable and consistent stream of revenue and cashflow from its long-term customer relationships. For instance, 1 in 2 of the nuclear fleet in the world receives services from Westinghouse.

Warren Buffet once shared that the three criteria he uses for evaluating a management are integrity, intelligence and energy – all 3 of which are characterized by Cameco’s management team. Cameco has a disciplined management team with a long-term mindset that has enabled the company to persevere through the doldrums of the nuclear industry’s lost years. When uranium prices are high, management had the self-restraint to not flood the market with uranium and correspondingly drive down prices. Instead, the company has been focused on long-term value creation by preserving its high grade, low-cost production assets by waiting for attractive long-term pricing. This has enabled the company to become well-positioned to take advantage of the current nuclear energy boom.

Amid rising global energy demand, Cameco is well-positioned to benefit from the growing need for nuclear energy for years to come. Since the ROCKLINC Partners Fund initiated its position in Cameco in February 2024, the stock has risen by over 45%. We plan to increase our stake as valuations become more attractive.

D. Moving Forward

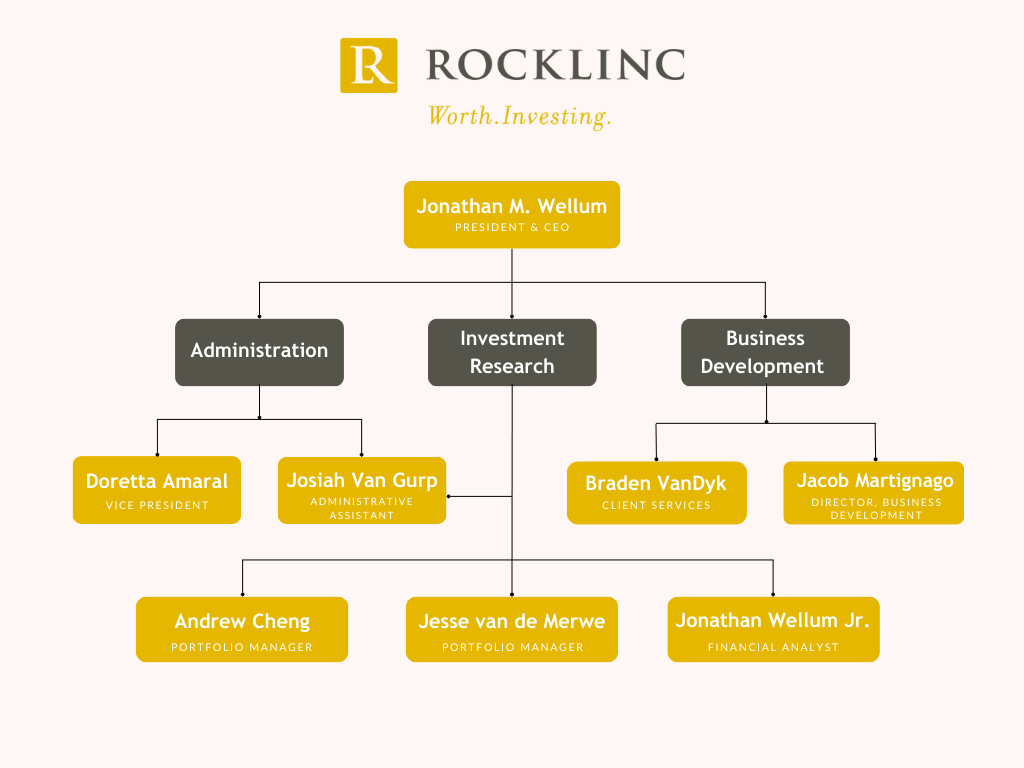

We continue to keep our eyes focused on the fundamentals of the businesses we invest in, within the context of a struggling global economy. We will do our best to take advantage of sharp moves in the market! We currently have eight full-time employees. Here is our organizational chart.

The investment team at ROCKLINC is diligently managing our portfolio companies to meet or exceed expectations while seeking new opportunities to enhance your investments. Despite tariffs, trade tensions, or military activities, our core strategy remains unchanged: building portfolios of exceptional businesses. Below are ten key principles guiding our approach:

- Patience: We wait for attractively priced opportunities, leveraging our cash reserves to buy low during volatile periods. Tariff-related uncertainty may create short-term noise but also long-term opportunities. Quality companies at compelling valuations reward investors who focus on fundamentals, not headlines.

- Monitor Central Banks: Monetary policies, including repressed interest rates and increasing money supply, significantly influence market valuations. The policies being pursued by Central Banks are not supportive of strong currencies.

- Address Unsustainable Deficits: Government deficits pose risks to purchasing power. We maintain significant positions in precious metals and hard assets to mitigate these risks.

- Diversify Strategically: Our focused portfolios (20-30 securities) are diversified across asset classes, sectors, and regions to balance risk and opportunity.

- Prioritize Strong Balance Sheets: We invest in companies with tangible assets, robust financials, and minimal counterparty risk.

- Focus on Essential Industries: We target firms in growing sectors with long-term secular trends, such as Cameco, our featured company this quarter.

- Avoid High-Risk Firms: We minimize exposure to heavily leveraged financial companies with complex balance sheets, such as banks and insurers.

- Maintain Liquidity: Adequate cash reserves allow us to capitalize on market dislocations, earning 2.5% – 4% annually while preserving flexibility.

- Stay Opportunistic: We remain positive and proactive, grounded in realism and truth.

- Anchor in Faith: We place our trust in enduring principles, as reflected in Philippians 4:6: “Do not be anxious about anything, but in everything by prayer and supplication with thanksgiving let your requests be made known to God.”

For questions about your account, please contact us to schedule an appointment.

ROCKLINC INVESTMENT PARTNERS INC.

Contact Information

ROCKLINC INVESTMENT PARTNERS INC.

4200 South Service Road, Suite 102

Burlington, Ontario

L7L 4X5

Tel: 905-631-LINC (5462)

www.rocklinc.com

| Doretta Amaral | damaral@rocklinc.com | (ext. 1) |

| Jonathan Wellum | jwellum@rocklinc.com | (ext. 2) |

| Jesse van de Merwe | jvandemerwe@rocklinc.com | (ext. 3) |

| Braden Van Dyk | bvandyk@rocklinc.com | (ext. 4) |

| Andrew Cheng | acheng@rocklinc.com | (ext. 5) |

| Jacob Martignago | jmartignago@rocklinc.com | (ext. 6) |

| Jonathan Wellum Jr. | jwellumjr@rocklinc.com | (ext. 7) |

| Josiah Van Gurp | jvangurp@rocklinc.com | (ext. 8) |

Disclaimer

The information contained herein reflects the opinions and projections of ROCKLINC (ROCKLINC) Investment Partners Inc. as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. ROCKLINC does not represent that any opinion or projection will be realized. All information provided is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. This communication is confidential and may not be reproduced without prior written permission from ROCKLINC.

- https://www.scientificamerican.com/article/california-faces-summer-blackouts-from-climate-

extremes/#:~:text=CEC%20Vice%20Chair%20Siva%20Gunda,free%20electricity%20supply%20by%202045. ↩︎ - https://www.world-nuclear-news.org/articles/meta-constellation-sign-20-year-clean-power-

deal#:~:text=A%2020%2Dyear%20power%20purchase,capacity%20at%20new%20US%20locations. ↩︎ - https://www.reuters.com/sustainability/climate-energy/meta-signs-power-agreement-with-constellation-nuclear-plant-2025-06-03/ ↩︎

- https://www.reuters.com/markets/deals/constellation-inks-power-supply-deal-with-microsoft-2024-09-20/ ↩︎

- https://www.cnbc.com/2024/09/20/constellation-energy-to-restart-three-mile-island-and-sell-the-power-to-microsoft.html ↩︎

- https://time.com/6342343/nuclear-energy-climate-change/ ↩︎

- https://www.aboutamazon.com/news/sustainability/amazon-nuclear-small-modular-reactor-net-carbon-zero ↩︎